What is cryptocurrency? In plain English: digital money that works without a bank or government sitting in the middle. That’s the short version. You’ve probably heard the word “crypto” thrown around in the news, in conversations, maybe in an ad with a celebrity holding a coin that doesn’t physically exist — and the rest of this article unpacks what it actually is, why anyone bothered to build it, and what you should be careful about, without hype and without pretending the risks aren’t real. When I first tried to understand crypto in 2017, every explanation I found was either trying to sell me something or written for people who already understood. This is the article I wish I’d had then.

TL;DR

- Cryptocurrency is digital money that works without a bank or government in the middle. Transactions are recorded on a shared public ledger called a blockchain.

- Bitcoin was the first one, launched in January 2009 by an anonymous person or group called Satoshi Nakamoto, partly as a response to the 2008 financial crisis.

- “Crypto” now covers a wide range of things: Bitcoin, Ethereum, stablecoins (pegged to the dollar), NFTs, and thousands of other tokens — not all of them serious.

- The appeal: you can send value across the internet without permission, and no single company can freeze your account.

- The risks are real: prices swing wildly, scams are everywhere, transactions can’t be reversed, and there’s no customer service line if something goes wrong.

What is cryptocurrency, exactly?

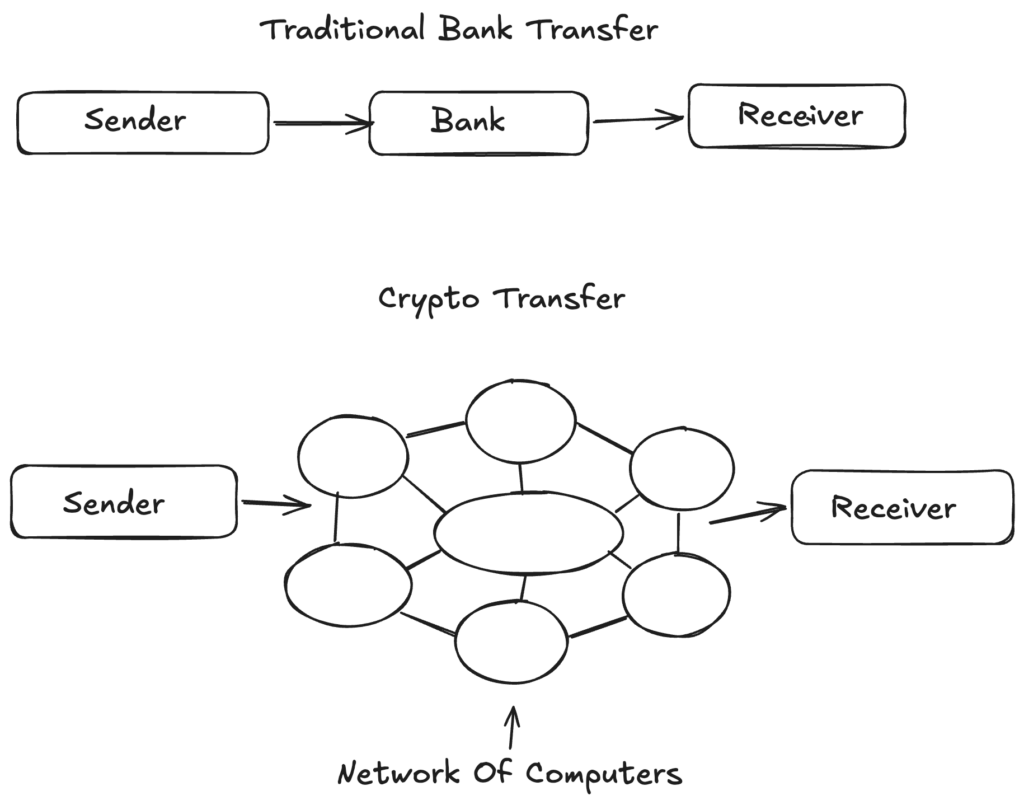

A cryptocurrency is a form of money that exists only as entries in a digital ledger — a kind of shared record book — that’s maintained by a network of computers around the world instead of by a bank.

When you send someone money through your bank, the bank updates its private ledger: subtract from your account, add to theirs. You trust the bank to do this honestly and to not freeze your funds. Cryptocurrency replaces that single trusted bank with a network of thousands of computers that all keep a copy of the same ledger and agree, through software rules, on what’s true.

That ledger is called a blockchain. It’s basically a shared spreadsheet that everyone on the network can read, but no one can secretly edit. Each new batch of transactions gets bundled into a “block” and chained onto the previous ones — hence the name. We’ll go deeper on how blockchains work in a separate article; for now, the takeaway is: it’s the mechanism that makes digital money work without needing a bank.

The “crypto” part of the name comes from cryptography — the math that secures the system. Your ability to send your coins is protected by a private key, which is essentially a very long password only you should know. If someone gets your private key, they can move your money. If you lose it, no one can recover it for you. That’s a big deal, and we’ll come back to it.

How crypto differs from regular money

The dollars in your bank account are what’s called fiat money — currency issued by a government and managed by banks. It works well for most things. You probably don’t lie awake worrying about whether your bank will lose your savings.

Cryptocurrency is different in a few specific ways:

No central issuer. No government prints Bitcoin. New coins are created by the network itself, according to fixed rules written into the software. Bitcoin, for example, has a hard cap of 21 million coins that will ever exist.

No central gatekeeper. Anyone with an internet connection can create a crypto wallet (a piece of software that holds your keys) and start sending or receiving. You don’t need permission, ID, or a credit check to hold it. That’s powerful — and also why scammers love it.

Borderless. Sending crypto from New York to Lagos works the same as sending it across the street. Same network, same rules, similar fees. International wire transfers through banks can take days and cost a lot; a crypto transaction usually settles in minutes to an hour.

Irreversible. If you send Bitcoin to the wrong address, it’s gone. There’s no support ticket. No chargeback. This trips up beginners constantly.

Pseudonymous, not anonymous. Your name isn’t attached to your wallet, but every transaction is public and permanent. Researchers and law enforcement have gotten good at tracing crypto flows.

Why would anyone want this? A few honest reasons: you live somewhere with an unstable currency and want to hold dollars (via stablecoins) without a US bank account; you want to send money internationally without paying remittance fees; you don’t trust your government or banks to leave your savings alone; or you just find the technology interesting. There are also less honest reasons — crypto is used for scams, ransomware, and sanctions evasion. Both are true.

Where cryptocurrency came from

Cryptocurrency has a real origin story, and it’s worth knowing.

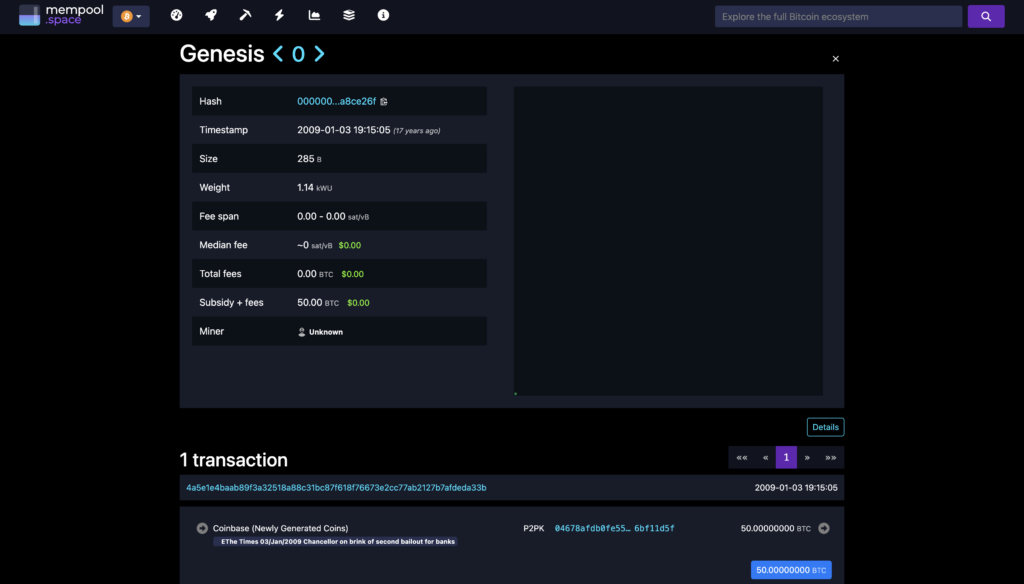

In October 2008, in the middle of the global financial crisis, an anonymous person or group using the name Satoshi Nakamoto published a nine-page document titled ”Bitcoin: A Peer-to-Peer Electronic Cash System.” It described a way to send money over the internet without going through a bank.

A few months later, on January 3, 2009, the Bitcoin network went live with its first block — the “genesis block.” Embedded in that first block was a line of text referencing a UK newspaper headline from that day: “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks.”

That message wasn’t an accident. Bitcoin was built, in part, as a reaction to a world where banks could be bailed out by governments while ordinary people lost houses and savings. The pitch was: here’s money that no government can print more of, that no bank can freeze, that no central authority controls.

Whether you find that compelling or not, it explains a lot about why crypto exists and why its early supporters were so ideological about it.

To this day, no one knows who Satoshi actually is. They stopped posting publicly in 2011 and have never moved their early Bitcoin holdings. That mystery is part of crypto’s folklore.

What “crypto” includes now

Bitcoin was the start, not the end. The word “cryptocurrency” today is a loose umbrella for a lot of different things, and it helps to know roughly what’s in the bucket.

Bitcoin (BTC). Still the largest by market value. Often described as “digital gold” — people mostly hold it as a long-term store of value rather than spend it on coffee. The original “digital money without a bank” story applies most cleanly here.

Ethereum (ETH). Launched in 2015 by a team led by a then-21-year-old Vitalik Buterin. Ethereum isn’t just digital money — it’s a platform where developers can build programmable applications (called smart contracts) that run on the blockchain. Most of the things people call “crypto apps” actually run on Ethereum or networks like it.

Stablecoins. This is where the “no bank, no government” framing starts to crack. Stablecoins like USDC and USDT are crypto tokens designed to always be worth one US dollar. They achieve that by being backed by actual dollars (or dollar-equivalent assets) held by a company. So you’re using a blockchain to move dollars around — fast and globally — but you’re trusting the company behind the stablecoin to actually hold those dollars. It’s a hybrid: crypto rails, traditional finance backing. Total stablecoin supply has grown to roughly $320 billion as of mid-2026 — larger than the foreign exchange reserves of countries like the United Kingdom or Canada. That’s how mainstream the technology has quietly become.

CBDCs (Central Bank Digital Currencies). These are digital currencies issued by governments — basically the opposite of Bitcoin’s original pitch. China has piloted one; other countries are exploring it. They use some similar technology but are very much controlled by a central authority. They’re often grouped under “crypto” in news coverage, but ideologically they’re a different animal.

NFTs (Non-Fungible Tokens). Tokens that represent ownership of a specific digital item — art, collectibles, in-game assets. The 2021 boom made them famous; the 2022–2023 bust made most of them nearly worthless. They use the same underlying blockchain technology but they’re not money in any practical sense.

Beyond these core categories, the crypto ecosystem now includes AI-related tokens, meme coins, decentralized AI projects, and DePIN (Decentralized Physical Infrastructure Networks). Each gets its own deeper treatment in our Coin Explainers section.

Thousands of other tokens. A lot of these are speculative, low-quality, or outright scams. The fact that something is “on the blockchain” doesn’t make it valuable or legitimate.

The real risks you should know about

I’ve been around crypto since 2017. I lived through a brutal bear market in 2018, watched the 2021 bull run get euphoric, then watched it collapse again in 2022. Here’s what I’d want a beginner to know honestly.

Prices swing violently. Bitcoin hit roughly $69,000 in November 2021 and fell below $16,000 a year later. Smaller coins routinely lose 80–95% of their value in bad markets. If you put money into crypto, you have to be genuinely okay with the possibility of losing most of it.

Scams are everywhere. Fake giveaways, fake support agents on Telegram, fake browser extensions, fake websites with one letter changed, “guaranteed return” investment platforms that vanish overnight. The FBI’s Internet Crime Complaint Center reported $9.3 billion in cryptocurrency-related fraud losses in 2024 — a 66% jump from 2023, covering everything from fake investment apps to hacked wallets and exploited DeFi protocols. If anyone DMs you offering crypto advice, assume it’s a scam until proven otherwise.

No consumer protection. If your bank account gets hacked, your bank usually makes you whole. If your crypto wallet gets drained, there is no equivalent. No one is calling you back. No insurance kicks in.

Transactions are irreversible. Send to the wrong address, send to a scammer, get tricked into signing a malicious smart contract — the funds are gone. This is the single biggest mental adjustment for beginners coming from the banking world.

You’re responsible for your own security. “Not your keys, not your coins” is a common saying in crypto. If you hold your own keys, losing them means losing your money permanently. If you let an exchange hold them for you, you’re trusting that exchange — and exchanges have collapsed before (FTX in 2022 being the most famous example). There’s a real tradeoff here, and we’ll write a whole article on it.

None of this means crypto is a scam. It means crypto comes with sharper edges than the financial system you’re used to, and you should know that going in.

Common questions

Is cryptocurrency real money?

It depends on what you mean by “money.” You can use it to buy things in some places, send it to people, and exchange it for traditional currency. Governments don’t classify it as legal tender in most countries (El Salvador is one notable exception, having adopted Bitcoin in 2021). In the US, the IRS treats crypto as property for tax purposes, not currency. So practically: yes, it’s real value. Legally: it sits in its own category.

Is cryptocurrency legal?

In most countries, yes — you can buy, hold, and sell it. Some countries (China being the biggest example) have heavily restricted or banned it. Tax rules vary widely. Always check your own country’s rules before you start.

Do I need to understand the technology to use it?

Not really, in the same way you don’t need to understand TCP/IP to use the internet. But you do need to understand the practical rules: keep your keys safe, double-check addresses, be skeptical of “opportunities,” and never invest more than you can afford to lose.

What’s the difference between cryptocurrency and Bitcoin?

Bitcoin is one specific cryptocurrency — the first and largest. “Cryptocurrency” is the broader category that includes Bitcoin, Ethereum, stablecoins, and thousands of others. All Bitcoin is cryptocurrency; not all cryptocurrency is Bitcoin.

Can cryptocurrency be hacked?

The major blockchains themselves (Bitcoin, Ethereum) have not been successfully hacked at the protocol level. But everything around them — exchanges, wallets, individual users — gets hacked constantly. The weak link is almost always people, not the underlying network.

Where to go from here

If this is your first real explanation of what cryptocurrency is, that’s enough to chew on for one sitting. You now understand the core idea — digital money that works without a bank or government sitting in the middle — and roughly what’s in the crypto ecosystem, where it came from, and what to be careful about.

A few topics we’ll cover next on Plainly Crypto, which build directly on this foundation:

- Bitcoin explained, going deeper on how the first cryptocurrency actually works and why it’s designed the way it is.

- Blockchain basics, unpacking the shared-ledger technology under the hood, in the same plain-English style.

- Wallets vs exchanges, explaining where your crypto actually lives, who holds the keys, and the tradeoff between convenience and control.

You don’t need to rush. The single best thing you can do as a beginner is take your time understanding the basics before putting any real money near this stuff. Crypto rewards patience and punishes hurry — and whatever you do put in, only invest what you can afford to lose.

A note on financial advice

Nothing on Plainly Crypto is financial advice. We write to explain how crypto works — not to tell you what to buy, when to buy, or how much to put in. Crypto is risky, regulations vary by country, and your situation is unique. Always do your own research, and if you’re putting real money in, consider talking to a qualified financial advisor in your country.