What is blockchain? In plain English, it’s a shared digital record-book that’s maintained by a network of computers instead of a single company or government. Nobody owns it, nobody can secretly edit it, and everyone using it sees the same history. That’s the whole idea — the rest is just plumbing.

If you’ve already read our overview of cryptocurrency and explainer on Bitcoin, this article completes the picture. Bitcoin made blockchain famous, but blockchain is the underlying technology — and it’s worth understanding on its own.

I’ve been using crypto since 2017, and blockchain was the concept that took me longest to actually click. Most explanations either skipped the technical bits entirely or buried me in computer science. This is the middle path I wish I’d had then.

TL;DR

- A blockchain is a shared ledger copied across many computers, with no central authority in charge.

- Transactions are bundled into “blocks,” and each block cryptographically links to the one before it — making the history extremely hard to tamper with.

- The network agrees on what’s true through a process called consensus. Bitcoin uses proof-of-work; Ethereum and many newer chains use proof-of-stake.

- Blockchain is not the same as Bitcoin, not the same as a database, and not the right tool for every problem.

- Real uses go beyond crypto — supply chains, settlements, digital ownership — but plenty of “blockchain solutions” from 2017–2021 were hype.

What is blockchain, in concrete terms?

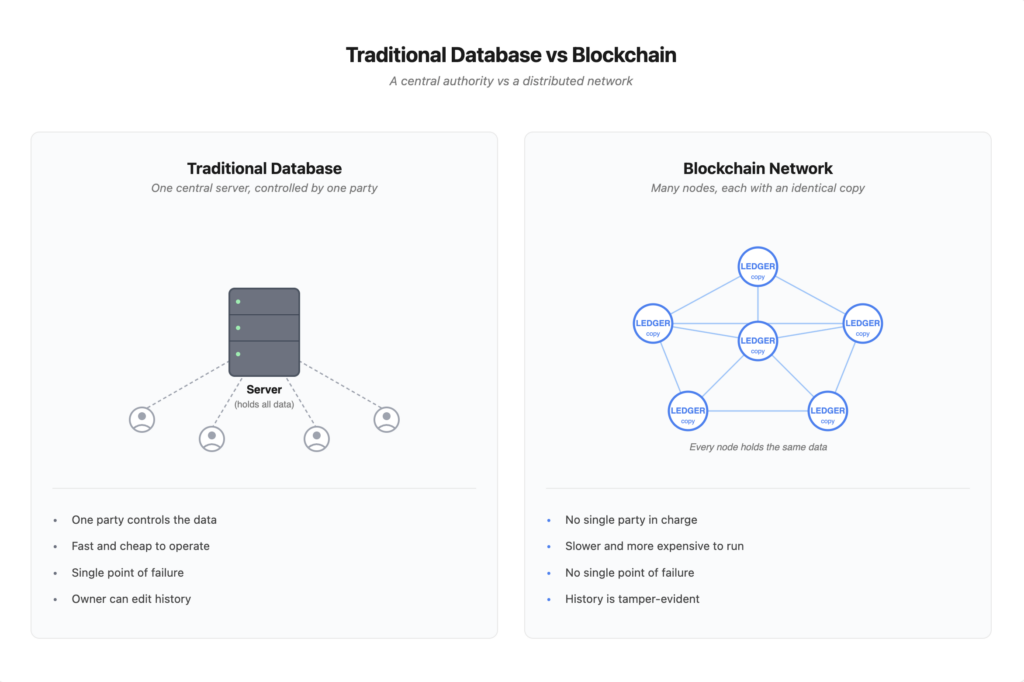

Picture a Google Sheet that lists every transaction ever made between a group of people. Now imagine that sheet exists as an identical copy on thousands of computers around the world. Anyone can read it. Nobody can secretly change an old row. To add a new row, the network has to agree the row is valid.

That’s a blockchain. A shared ledger — a record-book of transactions — maintained by a network of computers (called nodes) instead of a central authority like a bank.

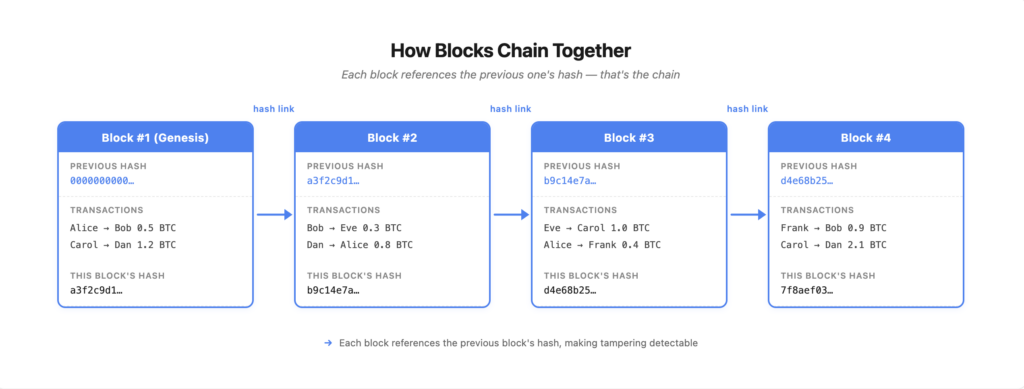

The word “blockchain” describes the structure of that ledger. Transactions aren’t added one by one. They’re collected into batches called blocks. Each new block points back at the previous block using a cryptographic fingerprint called a hash (more on hashes in a moment). String enough blocks together and you get a chain stretching back to the very first one. Hence: blockchain.

The breakthrough wasn’t any single piece of technology. Cryptographic hashes existed. Peer-to-peer networks existed. Digital signatures existed. The breakthrough was combining them so that strangers who don’t trust each other could still agree on a shared history without needing a referee in the middle.

That idea first appeared in a 9-page paper by an anonymous person or group calling themselves Satoshi Nakamoto, published on October 31, 2008. You can read the original Bitcoin whitepaper — it’s short and surprisingly readable.

How a block actually works

A block is just a container. Inside it, you’ll typically find:

- A list of transactions (“Alice sent 0.5 BTC to Bob,” and so on).

- A timestamp.

- A reference to the previous block — specifically, that block’s hash.

- A hash of the current block itself.

A hash is a number produced by running data through a mathematical function. Two important properties: the same input always produces the same output, but changing even one character of the input produces a completely different output. Hashes are also one-way — you can’t reverse them back to the original data.

Here’s why that matters. Each block contains the hash of the previous block. If someone tried to alter a transaction in block 500, the hash of block 500 would change. That would break the link with block 501, whose “previous hash” field still points to the old version. To get away with the change, the attacker would need to redo block 500, 501, 502, and every block after that — across thousands of computers, faster than the rest of the network can add new blocks.

In practice, that’s prohibitively hard on a mature blockchain. The chain isn’t impossible to tamper with, but it’s tamper-evident — any change leaves obvious fingerprints — and tamper-resistant in proportion to the network’s size.

How the network agrees on what’s true

If thousands of computers each hold a copy of the ledger, who decides which new transactions get added next? This is the consensus problem, and it’s where blockchains get interesting.

Consensus is a category of approaches, not a single mechanism. Different blockchains use different methods, each with its own trade-offs around energy use, security, decentralization, and speed.

Proof-of-work (Bitcoin’s approach)

Computers on the network — called miners — compete to solve a difficult mathematical puzzle. The first one to solve it gets to add the next block and earns a reward in the network’s cryptocurrency. The puzzle is hard to solve but easy for everyone else to verify, so the rest of the network can quickly check the answer.

It works. Bitcoin has run continuously since January 2009 using proof-of-work. The downside is energy: solving those puzzles requires enormous amounts of electricity, because security comes from the sheer cost of computation. Critics — fairly — point out that this is wasteful. Defenders argue the energy use is the security.

Proof-of-stake (Ethereum and many others)

Instead of computers competing with raw computing power, validators put up cryptocurrency as collateral — they “stake” it. The protocol picks validators (semi-randomly, weighted by how much they’ve staked) to propose and confirm new blocks. If a validator tries to cheat, they lose their stake.

Security here comes from financial risk rather than electricity. The energy cost is tiny by comparison.

Ethereum, the second-largest blockchain, switched from proof-of-work to proof-of-stake in an event called The Merge on September 15, 2022. Its energy use dropped by roughly 99.95% overnight. Cardano, Solana, and most newer networks also use proof-of-stake variants.

Other variants

You’ll come across names like Delegated Proof-of-Stake, Proof of Authority, and Proof of History. These are tweaks on the same core idea: how do strangers agree on what’s true without a central referee? Each variant makes a different trade. Some are faster but more centralized. Some sacrifice decentralization for throughput.

The honest takeaway: “blockchain” doesn’t mean one thing technically. The consensus mechanism shapes almost everything about how a chain behaves. I’ll cover proof-of-work versus proof-of-stake in more depth in a dedicated article.

What problem does this actually solve?

Two problems, really.

The double-spend problem. Digital files are easy to copy. If I send you a photo, I still have a copy. That’s fine for photos. It’s a disaster for money. Before Bitcoin, the only way to stop me from spending the same digital dollar twice was to have a central authority — a bank — track every balance. Blockchain solved this without a bank. The shared ledger records that I sent the coin to you, and the network won’t accept a second transaction trying to send the same coin elsewhere.

Removing the central authority. A bank can freeze your account. A payment processor can reverse a charge. A government can order a database changed. For most people most of the time, that’s fine — and often desirable. But it means trusting the institution in the middle. Blockchain offers an alternative: a system where the rules are enforced by software and math, not by a company.

Whether that trade-off is worth it depends entirely on what you’re using it for. Which brings us to the misconceptions.

What blockchain is not

A few things get muddled constantly. Worth straightening out.

Blockchain is not Bitcoin. Bitcoin uses a blockchain. So do thousands of other cryptocurrencies. So do some private corporate systems with no cryptocurrency at all. Bitcoin is one application of the technology, not the technology itself.

Blockchain is not a faster database. Regular databases are far better at almost everything databases do — they’re faster, cheaper, and easier to manage. Blockchain only makes sense when you specifically need a shared record between parties who don’t trust each other, with no single party in charge. If a company controls the system anyway, a normal database is the right tool.

Not all blockchains are energy-hungry. This one gets repeated as if it’s universal, and it isn’t. Proof-of-work chains like Bitcoin do use a lot of energy. Proof-of-stake chains use roughly 99% less. Lumping them together is like saying “all vehicles burn gasoline” — true for some, completely wrong for others.

Blockchain will not solve everything. Between roughly 2017 and 2021, every industry briefly had a blockchain pitch deck. Most of those ideas were solutions in search of problems. If your use case doesn’t actually need decentralization or trustless verification, blockchain just adds complexity and cost.

Public vs permissioned blockchains

Not every blockchain is open to the world.

Public blockchains like Bitcoin and Ethereum let anyone read the ledger, anyone send transactions, and anyone run a node. There’s no gatekeeper. Ethereum took this further by making the chain programmable — small programs called smart contracts run on it, enabling things like decentralized finance and NFTs. If you want a deeper sense of how that works, the Ethereum Foundation’s intro is a solid starting point.

Permissioned blockchains are private. Membership is controlled. Often used inside companies or between business partners — a group of shipping companies sharing cargo data, say, or banks settling trades among themselves. Hyperledger Fabric, hosted by the Linux Foundation, is the best-known framework here. There’s usually no cryptocurrency involved.

Both are technically blockchains. They serve very different purposes. When someone says “blockchain,” it’s worth asking which kind they mean.

Real-world uses, honestly assessed

Beyond cryptocurrency itself, where has blockchain actually proven useful?

Supply chain provenance. Tracking goods — coffee, diamonds, pharmaceuticals — from origin to shelf, with each handoff logged immutably. Walmart and Maersk have run real programs here. Useful where multiple parties don’t trust each other but need a shared record.

Cross-border settlements. Sending money internationally through traditional banks can take days. Some institutions now use blockchain rails for faster settlement between currencies. This is genuinely working, quietly, in the background.

Digital ownership and NFTs. A blockchain can record that a specific digital file belongs to a specific wallet. That’s what an NFT is — a record of ownership on a public ledger. The 2021–2022 NFT bubble produced a lot of nonsense, but the underlying mechanism — provable digital ownership — is real and still being used. NFTs get their own dedicated article in the Coin Explainers series.

Digital identity. Several governments and companies have experimented with putting identity credentials on blockchains. Promising in theory, complicated in practice. Mostly still in the pilot stage.

I spent years watching projects in 2017 and 2018 promise to “put X on the blockchain” — voting, real estate, music royalties, dentistry (yes, really). Most of them quietly disappeared. The ones that lasted tended to be the ones where decentralization actually solved a real problem.

What blockchain is bad at

Public blockchains come with real limitations, and they vary by consensus type.

Speed. Bitcoin’s base layer processes roughly 7 transactions per second — fine for high-value settlement, far too slow for everyday payments. The Lightning Network, a layer 2 built on top of Bitcoin since 2018, handles vastly more by routing payments through off-chain channels that only periodically settle to the main chain. Ethereum’s base layer handles around 15 per second, but layer 2 rollups like Arbitrum, Base, and Optimism now batch transactions off-chain at aggregate throughput exceeding 4,000 TPS — roughly 2 million transactions a day, which is where the bulk of Ethereum activity actually happens today. Visa, by comparison, can handle tens of thousands per second on a centralized network. Some newer chains like Solana are dramatically faster on the base layer itself, with their own trade-offs around decentralization and uptime. Layer 2 architecture is now standard for the major public chains — it pushes throughput much higher, but adds complexity.

Energy use (for proof-of-work). Bitcoin’s electricity consumption is comparable to that of a small country. That’s a real cost. Proof-of-stake chains don’t share this problem — worth knowing the difference.

Immutability cuts both ways. Blockchain’s strength — you can’t secretly change history — is also a weakness when something legitimately goes wrong. Send funds to the wrong address? No customer service line will reverse it. Get hacked? The thief’s transaction is just as valid as any other. Permanence is great until it isn’t.

Cost. Using a busy blockchain costs money — transaction fees can spike to uncomfortable levels when the network is congested.

These aren’t reasons to dismiss blockchain. They’re reasons to be specific about when it’s the right tool and when it isn’t.

Common questions

What is blockchain in simple terms?

A shared record-book of transactions, copied across many computers, with no single party in charge. Each new batch of transactions (“block”) links to the previous one using cryptography, so the history can’t be quietly changed. That’s the core — everything else (Bitcoin, Ethereum, NFTs, smart contracts) is built on top of that idea.

Is blockchain the same as Bitcoin?

No. Bitcoin runs on a blockchain, but blockchain is the broader technology. Thousands of cryptocurrencies use their own blockchains, and some non-crypto applications use permissioned blockchains with no cryptocurrency at all.

Can blockchains be hacked?

The core ledger of a major public blockchain has never been successfully altered. What gets hacked are the things around it — exchanges, wallets, smart contracts with bugs. The chain itself is generally secure; the surrounding software often isn’t.

Is anything on a blockchain truly anonymous?

Not really. Most public blockchains are pseudonymous — your real name isn’t attached, but every transaction your wallet makes is public forever. With enough effort, addresses can often be tied back to real identities. Some chains offer stronger privacy, but it’s a specialized area.

Do I need to understand blockchain to use crypto?

You don’t need to know how an engine works to drive a car. But understanding the basics will save you from a lot of bad decisions and bad pitches. The deeper you go into crypto, the more useful this knowledge becomes.

Will blockchain replace banks?

For most people, probably not entirely. Banks do many things blockchains can’t — and many people actively want the customer service, deposit insurance, and reversibility that banks provide. The more realistic future is that blockchain becomes infrastructure underneath some services, the way TCP/IP became infrastructure underneath the internet without most users ever thinking about it.

Where to go from here

You now have the foundational triangle: what cryptocurrency is, what Bitcoin is, and what blockchain is. From here, the natural next steps are how to actually hold crypto safely — covered in our upcoming Buying & Storing series — and a closer look at how the different consensus mechanisms compare in a future dedicated article.

One thing I’ve watched happen for years: people who rush into crypto get burned, and people who take a week to understand the basics tend to do far better. Crypto rewards patience and punishes hurry. There’s no prize for being early to a thing you don’t understand.

A note on financial advice

This article is for education, not financial advice. I’m sharing how blockchain works and what it’s used for — not telling you what to buy, hold, or do with your money. Crypto is volatile and risky. Only put in what you can afford to lose entirely, and make your own decisions based on your own situation.