Learning how to buy crypto safely is mostly about slowing down. The actual purchase takes a few minutes. Everything around it — picking the right exchange, surviving the identity check, dodging scams, deciding where to store what you’ve bought — is where beginners get hurt. There are hundreds of exchanges, thousands of coins, and an entire industry built around separating new buyers from their money. The good news is that a careful first-time buyer can avoid almost all of the common disasters with about an hour of preparation.

If you’re not yet sure what crypto actually is, start with what is cryptocurrency, then what is Bitcoin, then what is blockchain. Those three articles cover the “why” so this one can stay focused on the “how.” If you’ve already read them, you have more than enough context to keep going.

I’ve been buying crypto since 2017, which means I’ve watched two full bull-and-bust cycles and a lot of beginners get burned in both. The pattern almost never changes. People hear about crypto when prices are high, rush to buy, pick whatever exchange a stranger online recommended, send their coins somewhere they shouldn’t, and lose money to a mistake that would have been obvious with a little more time. The single most useful thing I can tell you is that the people I know who’ve done well in crypto are almost all the patient ones. The reckless ones either quit or got wiped out.

TL;DR

- Pick a reputable centralized exchange (Coinbase, Kraken, or Binance) that operates legally in your country. Avoid obscure platforms for your first buy.

- Expect to complete identity verification (KYC). It’s normal, legally required in most countries, and usually takes minutes to a couple of days.

- Fund with a bank transfer when possible — cheaper than card, much cheaper than credit card.

- Start small. $50–$200 you could afford to lose entirely. Your first purchase is a learning exercise, not an investment strategy.

- Bitcoin or Ethereum are the sensible first buys. Obscure altcoins are not.

- For anything beyond pocket change, move your crypto off the exchange into a wallet you control.

- If someone you don’t know is pitching you anything crypto-related, it’s a scam. Almost without exception.

The safety mindset: why most beginners get burned

Most first-time crypto disasters come down to four mistakes, and they happen in roughly this order.

Rushing. Someone reads an article, sees a price headline, panics that they’re missing out, and buys within an hour. They haven’t compared exchanges, haven’t decided what to buy, haven’t thought about storage. Fear of missing out is the most expensive emotion in crypto. The market has existed since 2009 and will exist next week. Taking three days to do this properly costs you nothing.

Wrong platform. A beginner ends up on a sketchy exchange because a YouTuber recommended it for the “bonus,” or because their country isn’t supported on the safer ones and they didn’t check. Or they download a fake app from an app store impersonating a real exchange.

Falling for scams. A “support agent” DMs them on Twitter after they tweet about a problem. A new friend on Instagram mentions a trading platform. A romantic interest on a dating app introduces them to a “guaranteed returns” opportunity. These scams work on intelligent people. They’re designed to.

Treating an exchange like a savings account. They buy crypto, leave it on the exchange for years, and then the exchange collapses (FTX in November 2022) or gets hacked or freezes withdrawals. The crypto is gone. They were never the owners in any meaningful sense — the exchange was.

The fix for all four is the same: slow down, verify everything yourself, never trust someone who contacted you first. Crypto rewards patience and punishes hurry. I’ve seen this play out enough times to say it without hedging.

CEX vs DEX — and why DEXes aren’t your starting point

There are two broad ways to buy crypto: centralized exchanges and decentralized exchanges. The difference matters.

A centralized exchange (CEX) is a company. It runs a website and app, takes deposits in regular money (USD, EUR, GBP, and so on), verifies your identity, and lets you buy and sell crypto on its platform. Coinbase, Kraken, and Binance are the most established examples. When you buy crypto on a CEX, the exchange holds it for you by default — much like a bank holds your dollars.

A decentralized exchange (DEX) is not a company. It’s a set of smart contracts — self-executing code — running on a blockchain. There’s no support team, no KYC form, no account. You connect a crypto wallet you already own, and the DEX swaps one crypto for another using automated pricing. Uniswap and PancakeSwap are the best-known examples.

DEXes are powerful, but they’re not where you start. Three reasons:

You can’t use one without already owning crypto, because DEXes don’t take regular money. The interface assumes you understand gas fees, slippage, network selection, and contract addresses — get any of these wrong and your funds can disappear. And mistakes on a DEX are usually unrecoverable. There’s no support line because there’s no support.

DEXes make sense later, after you have crypto already, some confidence with wallets, and a specific reason to use one (like buying a token that’s not listed on major CEXes — which is itself a reason for caution). DEXes get their own dedicated article later in the Buying & Storing series; we’ll cover the mechanics properly there.

For your first purchase, use a centralized exchange.

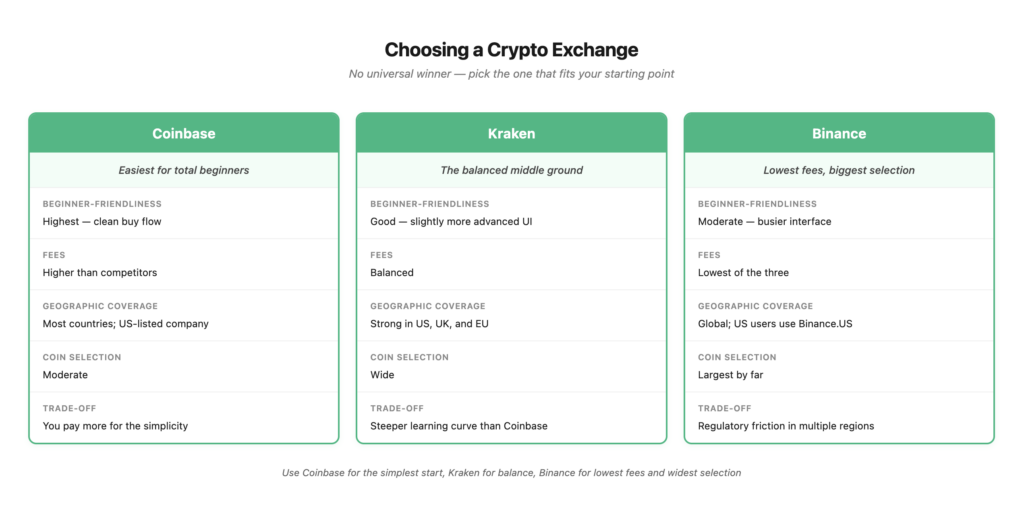

Comparing the safe three: Coinbase, Kraken, Binance

These three aren’t the only legitimate options, but they’re the ones I’d point a first-time buyer toward without hesitation. Each has clear trade-offs, and none of them is universally “best.”

Coinbase is the easiest for total beginners. The interface is clean, the buy flow is straightforward, and the company is publicly listed on the US stock exchange — which means a level of financial transparency you don’t get with private exchanges. Fees are higher than competitors, especially on the simple “Coinbase” buy interface (the “Advanced” view has lower fees but is less beginner-friendly). Available in most countries with some restrictions.

Kraken has been around since 2011, which makes it one of the longest-running exchanges still operating. It has a strong security track record, balanced fees, and solid coverage in the US, UK, and EU. The interface is slightly more advanced than Coinbase but still very usable for a beginner. It’s the option I tend to recommend to people who want a middle ground.

Binance is the biggest exchange in the world by trading volume. Lowest fees of the three, largest coin selection by far, and available in most of the world. The trade-offs: the interface is more complex, the company has had regulatory friction in multiple countries, and US users have to use Binance.US, which is a separate and more limited platform.

No winner. Use Coinbase if you want the simplest possible first experience. Use Kraken if you want balanced fees and a long security record. Use Binance if you want the lowest fees and largest selection and don’t mind a busier interface.

A quick note on Bybit, MEXC, KuCoin, Bitget

You’ll see these names a lot in crypto content, often promoted by influencers. They’re not appropriate first exchanges.

Bybit was hit by a hack of roughly $1.5 billion in February 2025 — the largest hack in crypto history. MEXC and similar platforms focus heavily on speculative altcoin listings, which is actively dangerous for someone whose first goal should be buying Bitcoin or Ethereum and learning the process.

These exchanges have legitimate uses for experienced traders, but for a first purchase they add risk you don’t need. We’ll compare them properly later in the series.

Account setup and KYC: what to expect

KYC stands for “Know Your Customer.” It’s the identity verification every regulated exchange runs you through. It exists because exchanges have to comply with anti-money-laundering laws to access banking systems. Without KYC, an exchange can’t process your bank deposit. With it, the exchange knows you’re a real person, which also makes it harder for scammers to operate at scale.

You’ll typically need three things: a government-issued photo ID (passport or driver’s license), proof of address (a recent utility bill or bank statement, usually within the last three months), and a live selfie or short video for biometric matching against your ID.

Processing usually takes minutes to a few hours. During market surges, when thousands of people sign up at once, it can stretch to one to three days. This is another reason to set up your account before you’re in a hurry to buy.

The common KYC mistakes that get applications rejected:

- The name on your ID doesn’t exactly match the name on your bank account (middle names, hyphens, etc.).

- The ID is expired.

- Your current address doesn’t match the address on the ID.

- Glare or shadows on the document photo make text unreadable.

Fix these before submitting and you’ll usually clear KYC on the first try.

Funding your account: bank transfer vs card

How you move money onto the exchange affects what you pay and how long it takes.

Bank transfer (SEPA in the EU, ACH in the US, wire elsewhere) is the cheapest option — often free or very low fee — and the most thoroughly verified. The downside is speed: it takes hours to a couple of days to settle. This should be your default.

Debit card is faster, often instant, but you’ll pay a 1–4% surcharge depending on the exchange. Fine for small first purchases where the convenience outweighs the cost.

Credit card is a bad idea. Many card issuers block crypto purchases outright. The ones that don’t usually code the transaction as a cash advance — which means high fees plus interest accruing from day one. You’d be paying interest on a volatile asset. Don’t.

Instant bank transfer options are increasingly common — SEPA Instant in the EU, FedNow in the US — and combine the speed of card with the low cost of a normal bank transfer. PayPal is supported on some exchanges and is fine as a convenience option, though usually not the cheapest.

Making your first purchase: a generic walkthrough

Exchange interfaces change every few months, so I’ll describe the process rather than specific buttons. The underlying flow is the same everywhere.

Find the buy or trade section. Select the cryptocurrency you want. Enter the amount in regular money — say, “$100” — and the exchange will calculate how much crypto that gets you at the current price. Choose market order for your first purchase. A market order buys at the current best available price and fills immediately. Limit orders, where you specify the price you’re willing to pay, are useful later but add complexity you don’t need today.

Review the fees, which the exchange will show you before you confirm. Then confirm.

The crypto will appear in your exchange account within seconds, sometimes a minute or two during heavy load. Clicking “buy” the first time feels weird — like you’ve done something irreversible and possibly stupid. That feeling is normal. You haven’t done anything dramatic. You’ve just bought a small amount of a digital asset.

What to buy first: the case for Bitcoin

If you’re buying crypto for the first time, buy Bitcoin.

Bitcoin has the largest market value of any cryptocurrency, the deepest liquidity (meaning you can buy and sell without moving the price), the longest track record going back to 2009, and the clearest story — a fixed supply of 21 million coins, no central issuer, no business model that can collapse. It’s also the asset with the lowest “is this a scam?” risk, and it’s now held by major institutions and even some governments, which gives it a legitimacy younger coins don’t have. What is Bitcoin covers the deeper reasoning.

Ethereum is a reasonable alternative. It’s the second-largest cryptocurrency, well-established, and powers most of the smart-contract economy. Either is a sensible first buy.

What you should not do is start with an obscure altcoin because someone online told you it was about to “moon.” Most small cryptocurrencies fail. Many are outright frauds — “rug pulls” where the creators vanish with the money. They’re illiquid, hard to research, and hard to recover from when they collapse. There will be time to explore the broader market later, after you understand what you’re doing. Your first purchase is not the place to take that risk.

The small-amount principle: start with $50 to $200 that you could afford to lose entirely. The purpose of your first purchase is to learn the process — sign up, verify, fund, buy, store. Whether the price goes up or down in the first month is irrelevant. Crypto is volatile, and your first hundred dollars is tuition.

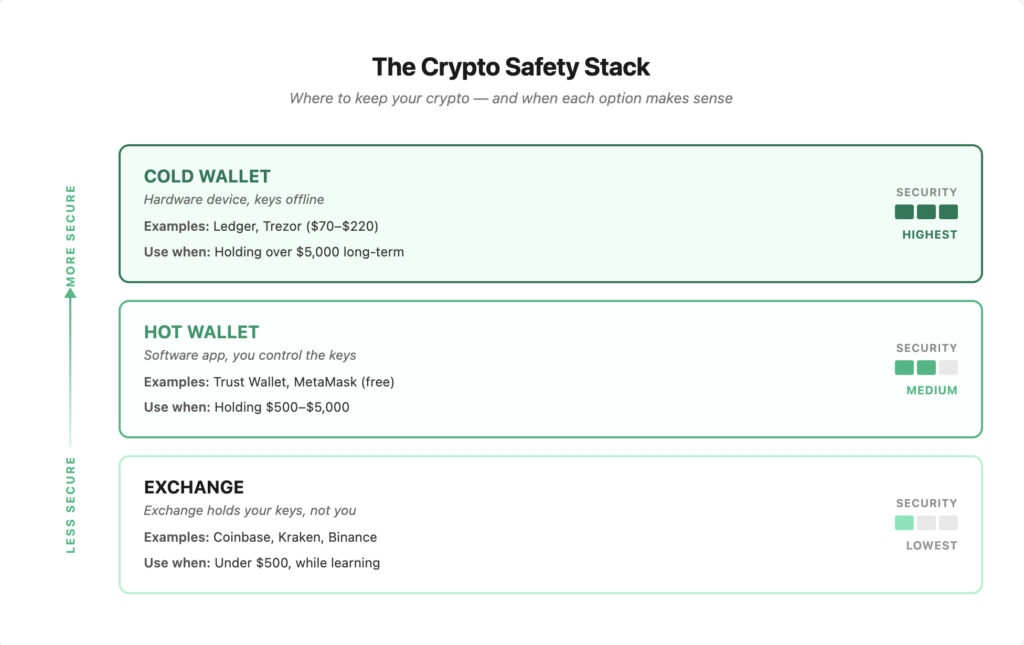

After the purchase: keep it on the exchange or move it?

There’s a phrase you’ll hear constantly in crypto: “not your keys, not your coins.” Here’s what it means in plain English.

When crypto sits in your exchange account, the exchange controls it. You see a number on a screen, but the actual cryptographic keys that let someone move that crypto are held by the exchange. You’re trusting them to keep the keys safe, stay solvent, not freeze your account, and let you withdraw whenever you want. History suggests that trust isn’t always warranted. FTX collapsed in November 2022 and many users lost everything. Celsius and Voyager went bankrupt the same year. Mt. Gox was hacked in 2014. Exchanges get frozen by regulators. They get hacked.

A hot wallet is a software wallet — an app on your phone or computer — where you control the keys. Trust Wallet and MetaMask are common examples; many exchanges also offer their own self-custody wallet apps. Hot wallets are free, easy to use, and you actually own the crypto. The trade-off is that they’re connected to the internet, which means a larger attack surface than offline storage. Best for small-to-medium amounts you might transact with.

A cold wallet is a physical device — a hardware wallet — that stores your keys offline. Ledger and Trezor are the two main brands; current models run roughly $70–$220 depending on which one you choose. The keys never touch an internet-connected device, even when you make a transaction. This is the highest level of personal security available to a normal user. Trade-offs: they cost money, they’re slightly less convenient, and you can lose the device physically (though you can recover access with a backup phrase, if you’ve stored it properly).

Rough decision framework (this is general guidance, not financial advice):

- Under $500: leaving it on a reputable exchange short-term is OK, especially while you learn.

- $500 to $5,000: move it to a hot wallet.

- Over $5,000: cold wallet. No exceptions worth making.

How to actually set up either type of wallet — including step-by-step recovery-phrase handling, which is the most important and most-botched part — gets a dedicated article in the Buying & Storing series.

Common scams to avoid

These are the patterns that account for the vast majority of beginner losses.

Fake exchange websites and apps. Scammers register URLs that look almost identical to real ones (binnance.com instead of binance.com, for example) and clone the design. They also publish fake apps that pass app-store review. Always type the URL yourself or use a bookmark. Always check the publisher on the app store.

“Customer support” DMs. You tweet about a problem with an exchange, and within minutes someone with a near-identical profile picture messages you offering help. Real exchange support never messages you first on social media. Ever. Anyone who does is a scammer.

“Guaranteed returns” pitches. Common on Instagram, TikTok, and dating apps. Often pitched as “trading platforms” or “mining programs.” Anyone promising guaranteed returns on crypto is lying. The asset is volatile by nature; nothing about it can be guaranteed.

Phishing emails. Emails that look like they’re from your exchange, asking you to “verify your account” or “confirm a withdrawal” via a link. Never click email links to financial services. Open a new tab and go to the site directly.

Pig butchering and romance scams. A long-game scam: someone starts a relationship with you — friendship or romantic — over weeks or months, then gradually introduces a crypto “opportunity.” These scams are sophisticated and devastating because by the time the ask comes, the victim trusts the scammer completely.

Recovery scams. Once someone has been scammed, predators target them again with promises to “recover” the lost funds — for an upfront fee. The funds are not recoverable. The “recovery service” is the same kind of scammer, often the same person.

The one rule that prevents nearly all of this: never send crypto to anyone you didn’t initiate contact with. No exceptions, no special cases.

A note on taxes

In most countries, buying crypto isn’t a taxable event — you’re just exchanging one currency for another asset. Selling crypto, trading one crypto for another, or earning crypto (through staking, mining, or work) typically IS taxable. Rules vary significantly by country, and they’re still evolving in many places.

Start keeping records from your first purchase: the date, the amount of crypto, the exchange you used, and the price you paid in your local currency. Most exchanges let you export this history later, but it’s much easier if you’ve already been tracking it. Future-you, possibly filing a tax return three years from now, will be grateful.

This is general information, not tax advice. For your specific situation, talk to a local tax professional who’s worked with crypto before.

Common questions

How much should I start with?

Whatever amount you’d be genuinely OK losing entirely. For most people, that’s $50 to $200 for a first purchase. The point of the first one is to learn the mechanics — not to make money.

Can I lose more than I invest?

If you’re just buying crypto and holding it, no. The most you can lose is what you put in. If you start using leverage, margin, or futures — which are not for beginners — you can lose more than your initial deposit very quickly. Don’t touch any of that for now.

Do I need to provide my real ID?

Yes, on any legitimate exchange. KYC is legally required in most countries. Exchanges that don’t ask for ID are usually either operating illegally in your jurisdiction or are scams. The friction is the point — it keeps the system safer for everyone.

What’s the difference between buying crypto and trading crypto?

Buying crypto means purchasing it with the intention of holding it. Trading means actively buying and selling to try to profit from price changes. Trading is a difficult skill, statistically unprofitable for most retail traders, and not what this article is about.

Can I buy crypto without an exchange?

Technically yes — through a few alternatives:

- Fiat on-ramp services like MoonPay, Ramp Network, and Transak let you buy crypto directly with a card or bank transfer and send it straight to a wallet address you provide. They’re often embedded inside crypto wallets (MetaMask, Trust Wallet) and DEX interfaces — so you’ll encounter them as “Buy Crypto” buttons even if you’re not actively looking for them. Convenient if you already have a self-custody wallet and just want to top it up; fees are higher than exchanges (typically 2–5%).

- Peer-to-peer platforms like Bisq and Hodl Hodl, where you buy crypto directly from another person.

- Bitcoin ATMs, physical machines that exchange cash for crypto. Fees are usually high (5–15%) and the machines have been targeted by scammers using QR-code coercion attacks.

- DEXes, but only if you already own crypto.

All of these have either higher fees, higher scam risk, or steeper learning curves than a centralized exchange. For a first purchase, use a centralized exchange. Once you have crypto and a wallet, on-ramps become useful for small top-ups.

What if my exchange gets hacked?

This is exactly why you don’t keep meaningful amounts on an exchange. Some exchanges have reimbursed customers after hacks. Many haven’t. If you wouldn’t trust a stranger to hold your money indefinitely, don’t trust an exchange to either.

Where to go from here

You now know how to buy your first crypto without making the worst common mistakes. The natural next steps are: learning how wallets actually work so you can move your crypto off the exchange properly, and understanding crypto market cycles so you have a realistic frame for the price movements you’re about to start watching. Both will get their own articles.

If you skipped them, what is cryptocurrency, what is Bitcoin, and what is blockchain are worth reading before you do much else. They’ll make every later article in this series easier to follow.

The pattern I keep coming back to, after enough years watching this market: the people who take a week to understand the basics before buying anything tend to do far better than the people who buy first and figure it out later. Crypto rewards patience. It punishes hurry. The market will still be here next Tuesday.

A note on financial advice

This article is education, not financial advice. Crypto is volatile and risky, and there’s no guarantee any specific cryptocurrency will hold its value. Only put in what you can afford to lose entirely. Make your own decisions based on your own situation, your own research, and ideally a conversation with a financial professional who understands your circumstances.